Small Business Saturday is an annual shopping event that takes place on the Saturday following Thanksgiving. Since 2010, the initiative has encouraged consumers to support local small businesses. The idea draws a stark contrast to Black Friday and Cyber Monday – two other big holiday shopping days that are dominated by mega corporations.

Small Business Saturday Supports Small Businesses

According to data highlighted by the U.S. Small Business Administration, Small Business Saturday drives as much as $17.9 billion in consumer spending at independent retailers and restaurants.

- Consumers have spent an estimated total of more than $120 billion at small businesses on Small Business Saturday over the past 10 years. (Bankrate, 2022)

- 53% of holiday shoppers plan to pay for at least some of their holiday purchases with a credit card. At the same time, more holiday shoppers will likely shop on Small Business Saturday than Black Friday this year. (Bankrate, 2023)

Small Businesses Rely on Credit Cards

Credit card payments provide small businesses with a raft of critical benefits: they enable customer convenience, enhance transaction security, and provide a stream of rewards that small businesses can reinvest in their operations. From facilitating quick and easy purchases to bolstering consumer confidence with robust security measures, credit cards are integral to the modern small business ecosystem. Rewards programs, in particular, often serve as a crucial financial lifeline, helping to offset operational costs and maintain cash flow.

- In 2022, card issuers spent an estimated $100 billion on cash back, rewards, and other credit card benefit programs. (Javelin Strategy & Research, 2023)

- The Federal Reserve Bank of Boston found that the average cash transaction is $22, while average non-cash transaction is $112. When a merchant begins accepting card payments, they experience a 10-15% increase in average transaction size. (Federal Reserve Bank of Boston, 2017)

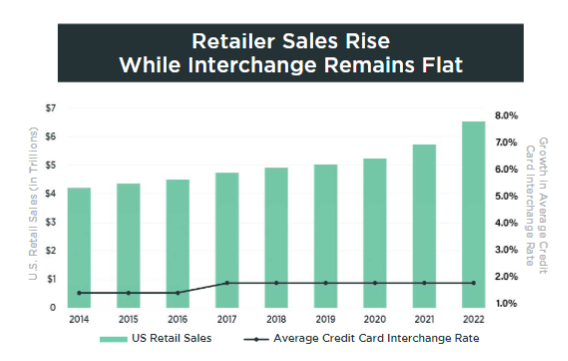

Cost of Using Credit Cards Has Remained Flat While Helping Drive Sales Growth

Interchange rates have remained flat over the past decade, all while adding significant value to merchants and consumers. Advancements in technology have made credit cards more convenient to use, with enhanced security and fraud protection measures that make credit cards payments safer and easier to process than handling cash.

- The rate of interchange has remained flat for the past seven years, as merchant sales have grown substantially. (Electronic Payments Coalition, 2023)

Durbin-Marshall: Unintended Consequences of Bad Policy

On June 7, 2023, several U.S. Senators and members of Congress introduced the so-called “Credit Card Competition Act” (CCCA) [S.1838/H.3881] in both the House and the Senate – where it is also known as the “Durbin-Marshall credit card/interchange bill.” The proposed legislation is a direct threat to our electronic payments and rewards system and would have a major negative impact on our local businesses, entrepreneurs, and tradespeople who use credit cards and rewards to run their businesses. It would circumvent the competitive free market with a government “routing mandate” that dictates which processing networks banks can accept, without regard to security or quality. All card issuing banks would be forced to open-up their credit cards to two payment processing networks, instead of just one that they know and trust.

- In 2021, economists reported that extending the Durbin Rule to credit cards could cause annual revenue losses of $5 to $10 billion for community banks and local credit unions. (Morning Consult, 2021)

- Half of small businesses “are concerned that future credit card regulation could lead to lower credit limits and thus a negative impact on their businesses.” (Cornerstone Advisors, 2023)

- Despite making up only 11.7% of the credit card population, lower-income and low credit households would lose $434 million, close to 22% of the cost borne by all consumers if the CCCA is enacted. (Amsterdam News, 2022)

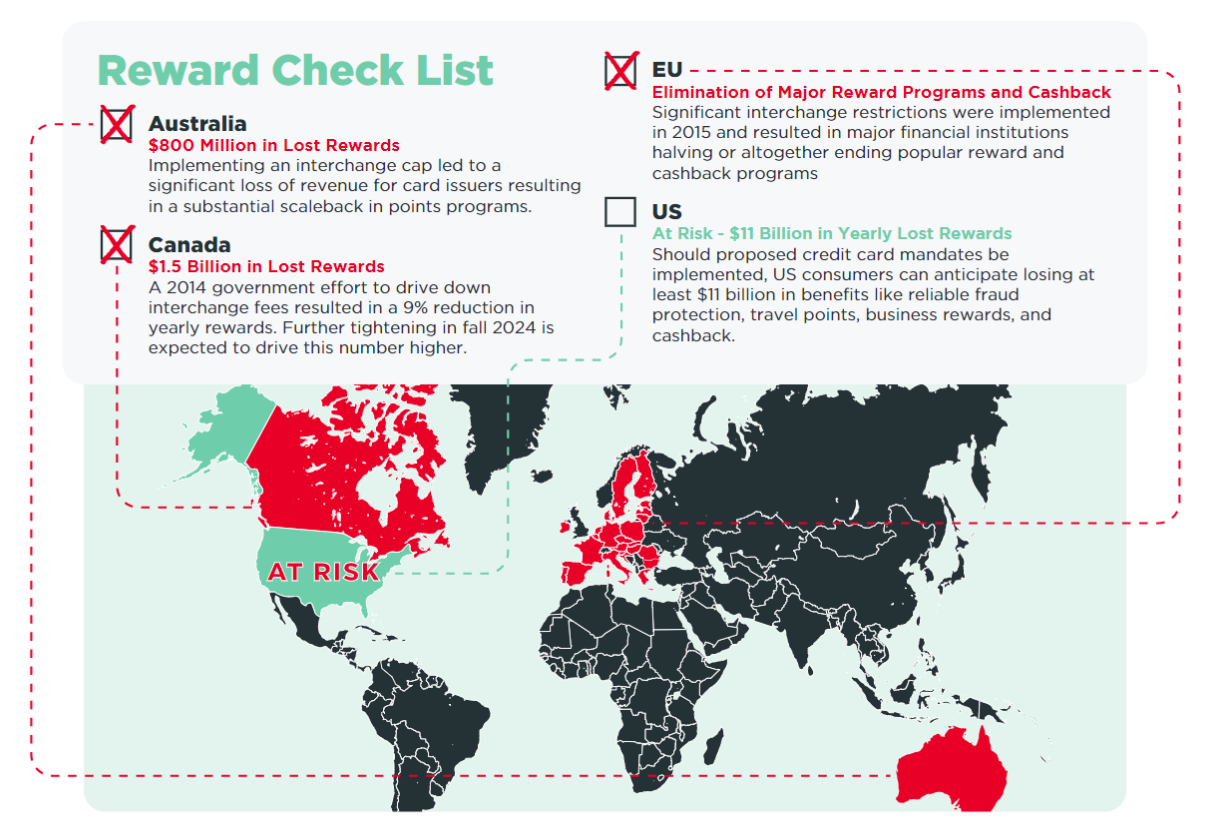

- In Australia after the Reserve Bank added Durbin Amendment-style regulations to credit that limited interchange fees, the value of rewards points fell nearly 25%. (CRA International)

- Credit card interchange reductions that significantly reduced rewards programs in the European Union, Australia and Canada are a warning of what’s to come in the U.S. should CCCA become law. (International Center for Law & Economics)

Interchange Mandates Didn’t Work the Last Time They Tried It

You don’t have to look far for historical evidence of how Durbin-Marshall will negatively impact small businesses. In 2010, Congress passed a similar provision that forced price controls on debit card processing. That legislation only increased big box retailer revenue, while studies show little to no cost savings were passed on to consumers or small businesses. Because many alternative payment processors charge a 3.5% flat fee, savings never made their way to small businesses. Instead, small businesses and consumers saw reduced availability of free checking, higher monthly fees and minimum account balances – and the disappearance of debit card rewards programs.

- Customers did not see lower prices. According to the Federal Reserve Bank of Richmond, 77 percent of retailers failed to lower prices and 21 percent actually increased prices after routing mandates went into effect. (Federal Reserve Bank of Richmond, 2014). Meanwhile, a University of Chicago report found that instead of saving money, the Durbin Amendment indirectly lost consumers between $22 and $25 billion. (University of Chicago, 2013)

- The Durbin Amendment had limited and unequal effects on merchants in terms of lowering costs for merchants. Averaging across 26 sectors, 89.9% of all merchants had experienced either no change in debit costs or had seen their debit costs increase under the new legislation. (Federal Reserve Bank of Richmond, 2015)

- In 2022, a Government Accountability Office study found that after the Durbin Amendment, free checking at banks targeted by the amendment declined by 35% and by 15% at “exempt” banks. (Government Accountability Office, 2022)

- In 2014, researchers at George Mason University reported that the Durbin amendment increased the unbanked population by one million Americans (primarily in low-income communities). (George Mason University, 2014)

- In 2011, a study found that the availability of debit card rewards fell 30% in the year following the implementation of the Durbin Amendment. (Bankrate, 2011)

Conclusion

Every year on Black Friday, mega corporate retailers advertise crazy deals that are rarely as good as they seem – and that’s exactly what’s happening with Durbin-Marshall. Misguided politicians are making the same promises they did back in 2010, forcing government mandates onto small businesses in an attempt to fix an electronic payments and rewards system that isn’t broken. This year, Congress should take inspiration from Small Business Saturday and say no to Durbin-Marshall.