The Holiday Season is in full swing and as consumer spending rises, so too do fraud attempts. According to a 2022 study by AARP, three out of four U.S. adults age 18-plus have been targeted by or experienced at least one form of fraud. Fortunately, more and more consumers and merchants are using credit cards to protect themselves against financial losses. In 2021, our electronic payment system stopped $80 billion in fraud attempts, thanks in part to the interchange funds that payment networks and card issuing banks use to protect consumers and merchants through investments in security technology, including EMV chips, contactless cards, and biometric authorization.

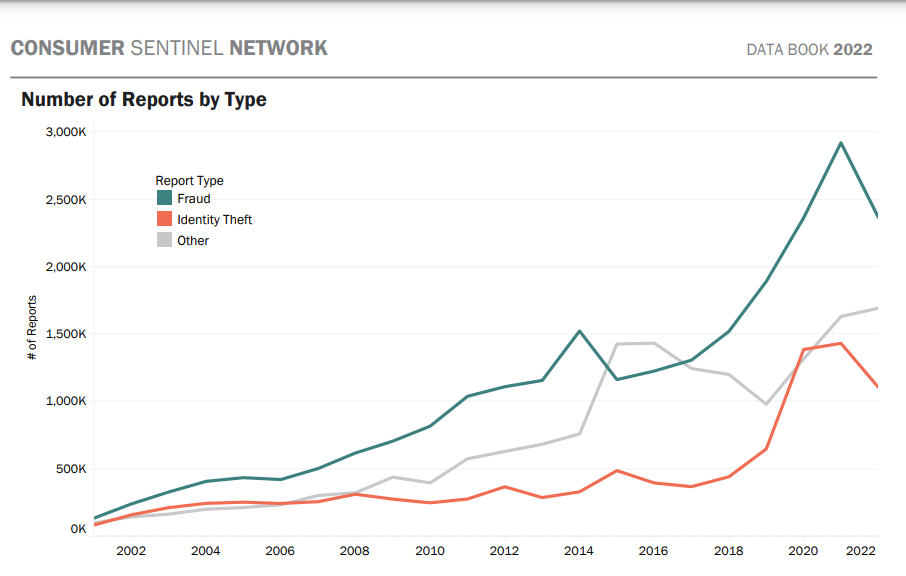

Above: Consumer Sentinel Network 2022 Data Book consumer fraud reports.

Credit Cards Offer Secure Transactions with Zero Liability

Part of the electronic payment system’s interchange funds go towards investing in safe transactions by acquiring security technology, including EMV chips, contactless cards, and biometric authorization that protects consumers and merchants from fraud. Payment networks and card issuing banks use these investments to support data security, programs for rewards, innovation, and more. This includes rapid alerts that let you know someone may be trying to use your credit card for theft or fraud.

Why the Credit Card Competition Act (CCCA) Hurts Small Businesses

If the new mandates in the Durbin-Marshall credit card bill are enacted, the peace of mind Americans enjoy with credit card transactions could be over as we know it. The bill would require credit card transactions to be processed on at least two networks, with one of them being a smaller, less well-known entity — many of which haven’t invested in the financial security systems needed to protect consumer information.

Senator Durbin passed his original Durbin Amendment in 2010, which imposed similar routing mandates on debit cards. This contributed to the fraud rate for debit cards increasing by MORE THAN 120% in subsequent years. A similar outcome for credit cards would likely cost OVER $6 BILLION in additional fraud.

Small Businesses Won’t See Any Costs Savings

Small businesses are the lifeblood of our economy, but would receive none of the cost savings of Durbin-Marshall. Half of cyberattacks today target small businesses, costing them on average $200,000. Small businesses could also be subject to liability if banks become unable to cover the cost of fraud and customer disputes. The nonpartisan Congressional Research Service recently stated, “it is unclear who would benefit” from the legislation.

Fraud Protection & Cybersecurity Will Decline

Financial services companies frequently bear the cost of fraud to ensure that consumers can be confident using credit cards. They also spend billions of dollars each year to bolster cybersecurity, leading to technological advancements like tap-to-pay and contactless payments. But under the CCCA, providers wouldn’t have the interchange revenue to invest in the protections and innovations that cardholders deserve.

New Mandates Will Stifle Innovation in the Credit Card Market

Forcing consumers, banks, and small financial institutions to have their cards processed on other networks would require reissuing credit cards to all cardholders. This change alone would cost billions of dollars and cause mass disruption to consumers and small businesses, forcing credit card networks and issuers to cede their routing technology to their competitors, disincentivizing investment in payments security and innovation.

Consumer Security will be Threatened

Durbin-Marshall destroys consumers’ trust and financial protection. It mandates that the secure payment technologies be handed over to unknown, untrusted companies who may not have invested in consumer safety, eroding decades of security advancements. If there’s ever a security issue with these alternative networks, consumers and small businesses would not have the same protections they have come to expect today. The legislation is a race-to-the-bottom in card security, leaving consumers vulnerable to the lowest-bidding, least secure networks. This is not competition, it’s a cybersecurity crisis in waiting.

Potential for Corporate Mega Stores to Mix Commerce and Banking

The nonpartisan Congressional Research Service recently highlighted a number of unintended consequences with the legislation, including the potential for corporate mega stores to create their own payment networks which would hurt small businesses. “There is nothing stopping the major retailers from creating a payment network … this would tighten links between commerce and banking and potentially lead to conflicts of interest.”

Conclusion

Durbin-Marshall is a threat to security in our electronic payments system. The bill will force the use of untested alternative payment networks that may skimp on security features. At the same time, it will reduce funding for fraud protection and innovative security features, and every credit card will need to be reissued.

As holiday shopping season kicks into full swing, small businesses across the country will be feeling the benefits of a safe, secure electronic payments system. The message from small business owners to Congress is clear: don’t let the corporate mega stores play grinch this holiday season. Protect consumer security and preserve the electronic payments system.