I. INTRODUCTION

Credit cards are very popular among U.S. consumers. By year-end 2024, there were 608 million open general purpose card accounts, a 35% increase since 20181. More than 80% of U.S. adults have a credit card account in their name2. In 2024, credit cards generated $6.5 trillion in purchase volume3, and industry estimates suggest that nearly three-quarters of all nationwide retail sales come from credit card transactions4.

Despite the importance of credit cards in driving revenue, retailers often complain about the costs associated with accepting them as payment. Retailers pay an average of 2.3% on each credit card transaction to card issuers, payment networks, and acquirers that collectively facilitate the payment5. This cost, known as the merchant discount rate or MDR, consists of several components, including interchange fees, network fees, and acquirer / processor fees.

Importantly, accepting other forms of payment is not costless. Indeed, IHL group, a global research and advisory firm specializing in technologies for the retail industry, estimates that the average cost to process and handle a cash transaction is 9.1% of the sale amount6. Bank of America estimates that business checks can cost between $4 and $20, depending on the price of the check and shipping, and the time employees spend writing, mailing, collecting, and reconciling the check7.

Processing debit cards also incurs certain costs, though on average, the costs are cheaper compared to credit cards. This is due, in part, to government-imposed price caps on interchange fees. The Durbin amendment was established in 2010 and capped debit card interchange at $0.21 per transaction for banks with $10 billion in assets. The price cap has had a negative effect on both consumers and debit card issuers: according to the most recent Federal Reserve data, more than 80% of debit card issuers lose money on every debit card transaction8, while consumers have experienced a sharp decline in the availability of debit card rewards programs and free checking, as well as higher minimum balance requirements and higher fees9. Merchants were supposed to pass on savings from the legislation to consumers, but after 15 years of evidence, a litany of economic studies have concluded that this has not occurred in practice10, 11.

Despite the failed experiment of the Durbin Amendment, retail industry lobbyists continue to press for price controls on credit card interchange, either through direct government-imposed price caps or through indirect means that achieve the same effect. These efforts are all based on the same flawed argument that merchants are paying “too much” to accept credit cards. But how much is too much? A typical approach would be to assess the level of competitiveness in the market; by this measure, the evidence suggests that the credit card industry is highly competitive12,13. Another approach is to compare the price of a service to the value it provides the buyer — in short, to determine whether the benefits exceed the costs.

To this end, EPC conducted an analysis to quantify six distinct ways in which merchants benefit from accepting credit cards. Using these estimates, EPC develops an illustrative example of three restaurants that exclusively rely on different types of payment and quantifies the extent to which restaurants benefit from accepting credit cards. Finally, EPC reviews the National Association of Convenience Stores’ most recent “State of the Industry” report to gauge the extent to which top performers in the convenience store industry depend on credit cards for their success.

II. Quantifying the benefits Merchants Receive by Accepting Credit Cards

II. Quantifying the benefits Merchants Receive by Accepting Credit Cards

II.1 Increased Sales Revenue

- Credit cards make up 40% of transaction volume, five percentage points higher than the next closest payment method, debit cards.17

- Credit cards are the most popular payment instrument: 35% of all payments are made with a credit card, also five percentage points higher than the next most popular payment, debit cards.18

II.2 Increased Revenue Generated by Merchant-Branded Cards

Some large retailers create partnerships with card-issuing banks to issue co-branded or private-label cards. These cards carry the retailer’s brand and usually grant discounts and/or rewards for consumers that shop at the given retailer. The co-issuing bank is typically responsible for credit operations, including managing credit lines and providing customer service, while the retail partner manages the loyalty and benefits program, markets the card, and hosts the application process.25 These cards drive significant sales for retailers, who also typically receive a share of the fees and interest collected by the card issuer, as well as lump sum partnership payments, including multi-million dollar signing bonuses.26

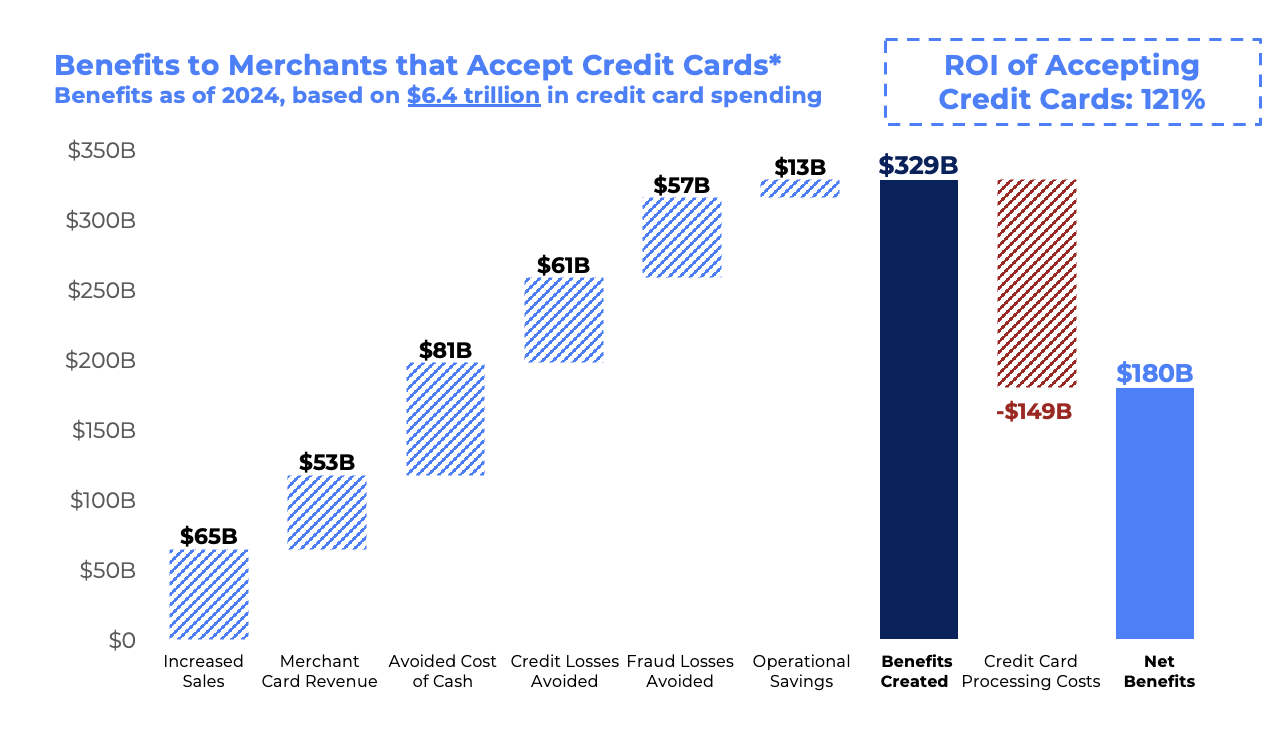

Per the Consumer Financial Protection Bureau (CFPB), from 2018 – 2023, retail credit cards accounted for an average of 8% of gross profits for major retailers with a card program.27 EPC defined major retailers as the 100 largest retailers in the country by sales volume as reported by the National Retail Federation.28 EPC summed up U.S. sales for all major retailers that offered a credit card and then applied an estimated gross margin of 30%.29 Once gross profit was calculated, EPC applied the CFPB’s 8% share to calculate the approximate revenue generated by the top 100 retailers in the U.S. that offer a card program: $53 billion.

II.3 Avoided Cost of Cash

Unlike credit cards, accepting cash does not produce a paper trail: merchants do not receive monthly statements detailing cash transactions or the costs associated with accepting those payments. As a result, many merchants assume accepting cash is free, or at least cheaper than accepting credit cards. In reality, processing and handling cash is quite costly. The costs of cash acceptance can include the time and labor needed to count and reconcile tills, audit discrepancies, open cash drawers and rebuild for next cashier, transport deposits at a nearby bank, and losses from theft or miscounting.30 The cost of cash varies by industry: for a restaurant, the cost of cash is 15.5%, but for a grocery store, it is 4.7%.31 On average, it costs merchants 9.1% of each cash transaction to handle and process the payment.32 In contrast, the average cost of processing a credit card payment (including interchange, network, and acquirer costs) is 2.3%.33 As a result, as the share of transactions comprised by credit cards rises and the share comprised by cash falls, merchants’ payment-handling costs are reduced.

To quantify the avoided cost of cash and corresponding benefit to merchants, EPC compared the observed total cost of cash in the economy to a counterfactual economy in which credit cards are not accepted. Data from Nilson indicates that cash currently makes up around 8.3% of transaction volume, whereas credit cards make up 40%.34 Using an estimated cost of cash of 9.1%, current cash processing costs for retailers are approximately $121 billion on total transaction volume in the economy [total cash processing costs are lower than total credit card processing costs because there are significantly less cash transactions in the economy compared to credit card transactions. The Federal Reserve notes that 35% of all payments are made with a credit card, compared to 14% with cash.35 The average credit card transaction costs issuers 2.3%, while the average cash transaction costs 9.1%].

To model a counterfactual world without credit cards, this analysis assumed that transactions currently paid with credit cards would shift to other payment methods in proportion to their existing non-credit shares. This assumption implies that cash absorbs the same share of displaced credit card transaction volume as it currently does of non-credit transaction volume (13.8%), such that the total cash transaction volume in the counterfactual scenario is equal to the existing cash volume plus the new portion of former credit card volume that shifts to cash. Using the same IHL estimate for the cost of cash, processing and handling costs on this new cash transaction volume is estimated at $201 billion. The avoided cost of cash is the difference between merchant cash-handling costs in the current economy and merchant cash-handling costs in the counterfactual economy, approximately $81 billion.

II.4 Avoided Credit Losses

When a customer uses a credit card, the merchant typically receives payment within 1 – 3 business days. In contrast, issuing banks do not experience immediate repayment every time a credit card is used; instead, banks must wait until the end of the billing cycle to collect payment. This dynamic ensures that credit card issuers, not merchants, take on the credit risk when a customer pays with a credit card. When banks write off credit card balances as uncollectible, those dollars have already been paid to merchants. Therefore, the credit losses absorbed by card issuers directly translate into the credit losses avoided by merchants.

A charge-off is the accounting term used for an uncollected payment a creditor writes off as a loss because they do not expect to receive repayment. In 2024, the value of net charge-offs from Visa, Mastercard, American Express, and Discover on credit card payments was $61 billion.36 For a merchant, this value represents a benefit as it is the dollars already received because a customer used a credit card and the issuer, not the merchant, absorbed the credit risk involved with the transaction.

II.5 Avoided Fraud

Credit card issuers and networks invest heavily in advanced technology every year to protect consumers and merchants against fraud. While fraud still occurs in the credit card market, these investments detect and prevent billions of dollars in fraudulent transactions each year. By accepting credit cards, merchants are protected by the fraud-prevention strategies issuers and networks put in place. Detected and prevented fraudulent transactions and the corresponding dollars lost from those potential transactions represent the avoided potential loss for merchants. Without the card networks’ protections, fraudulent transactions would have otherwise been processed and would likely result in merchants losing the value of the transaction and/or incurring costs to recoup the fraudulent payment.

Visa reported that it blocked $40 billion in attempted fraud in 2024,37 while Mastercard reported that it prevented $50 billion in fraud losses over the past three years ($16.7 billion per year).38 Summed together, the $57 billion in fraud prevented is a benefit to everybody that participates in the credit card market, including merchants.39

II.6 Reduced Costs Due to Operational Efficiencies

For business-to-business (B2B) transactions, organizations will often accept payment types that are less commonly used by consumers, such as ACH or check. These payment methods come with their own benefits and costs, including the resources and time required for acceptance and processing. As mentioned in the introductory paragraph, a business check can cost between $4 and $20 to send and process depending on the price of the check, shipping fees, and the opportunity cost that is spent writing, mailing, collecting, and reconciling the check.40 A firm that accepts credit cards over ACH or check payments will experience operational efficiency improvements when setting up new customers, reconciling payments, and administering fraud-related tasks.41

- New Customer Setup. When a business accepts ACH or check, they generally have to set up a new customer, incurring authorization, verification, or new enrollment fees from a bank.42 For ACH payments, staff might have to validate account and routing information and secure explicit customer consent through written documentation.43 The operational, labor, and administrative costs are significantly reduced or eliminated entirely for credit card transactions.44

- Payment Reconciliation Efficiencies. ACH and check payments often provide little information on what the payment is for, require manual effort to enter payment information into a system, and time to settle and clear. This often leaves businesses with missing information on customer payments, requiring businesses to complete payment reconciliation and audits.45 In contrast, accepting a credit card ensures that a company has clearer information on payment activity in real time, and can trust in the veracity of the transaction protected by card networks and issuers.

- Fraud-Related Administrative Tasks. Accepting ACH or check payments requires the merchant to handle potential fraud associated with those payments. Being responsive to fraud means a merchant might have to review and sign affidavits documenting that fraud occurred, and/or help customers that fall victim to a fraud attempt.46 These administrative tasks require time and labor and prevent the merchant from focusing on their core business. Compared to ACH and check, credit cards have more robust security measures in place, including real-time monitoring by financial institutions for irregular activity, quick reversal of unauthorized charges, and more comprehensive authorization processes.47 As such, accepting credit cards reduces the fraud-related administrative burden merchants face compared to accepting ACH or check payments.

For this benefit calculation, this analysis used a similar framework outlined by the consulting firm Forrester in their study titled: “The Total Economic Impact of Commercial Credit Card Acceptance.”48 In that study, Forrester calculated that a composite organization (a hypothetical organization created by Forrester based on a survey of merchants and certain assumptions about the B2B market) saves about $2.3 million in process efficiencies in the first year it replaces older payment types (e.g., ACH payments and checks) with credit cards. As a share of the firm’s credit card sales in that same year, process efficiencies made up 0.46%. The CFPB reports that in 2024, purchase volume on consumer credit cards equaled $3.6 trillion.49 In total, credit card purchase volume in 2024 was $6.5 trillion,50 suggesting that the B2B credit card market was roughly $2.9 billion. Applying 0.46% to total B2B c

III. Total Benefits

IV. NACS Findings

To corroborate the findings from the benefits of credit cards analysis, EPC reviewed the National Association of Convenience Stores’ 2024 State of the Industry report.52 The report provides an overview of the financial performance of the convenience store industry and a more specific breakdown of the finances among the top 10%, bottom 10%, and average performing stores. The report provides the following highlights:

- Card processing costs increased 7.1% for the industry from 2023 to 2024. However, the report attributes the rise in card processing costs to rising fuel prices, increased pump transaction, and heightened credit card usage, and not an increase in the actual fee as the reason for elevated processing costs.53

- More than 80% of transacted dollars in the industry were made by card, compared to around 19% in cash. On a transaction volume basis, around 70% of transactions were conducted via a payment card. Customers used cards to pay for larger items and relied on cash for smaller transactions.54

- As a share of total gross profit, card processing costs decreased 30 basis points from 2023 to 2024 (7.8% to 7.5%) despite total gross profit increasing 4.1% over the same time frame.55 This suggests that card processing costs do not detract from profits — instead, (and as evidenced in the following section), greater card usage actually contributes to larger profits.

Comparing the top 10 percent of stores with both average and bottom-performing stores shows a clear pattern: stores with higher sales pay more in card processing costs and earn substantially higher profits. This is not surprising, since card processing costs are assessed as a percentage of sales — firms that sell more using cards will naturally have higher processing costs. What is notable, however, is that higher card processing costs are associated with much greater profitability. The top 10 percent of stores pay card processing costs that are roughly 2.5 times higher than those of the bottom 10 percent, yet their profits are 13 times greater.56 A similar relationship holds when comparing top-performing stores to the average: while card processing costs are nearly twice as high, profits are also nearly twice as large.57 These data indicate that card acceptance costs do not erode profits; rather, they reflect increased card-driven sales that more than offset the costs. In short, the stores that pay the most in card processing costs are also the most successful in terms of both sales and profitability.

V. Restaurant Example

As a final demonstration of the benefits provided to merchants that accept credit cards, EPC developed an illustrative hypothetical of three restaurants that offer different payment options. Restaurant A accepts cash only, Restaurant B accepts both cash and credit cards, and Restaurant C accepts credit cards only. The construction of the hypothetical restaurants follows data from the Federal Reserve, which shows that, on average, consumers make 7 in-person credit card payments and three cash payments at a restaurant in a given month.58 Using this finding and the assumption that each restaurant receives 10,000 monthly payments with an average cash transaction of $25, the following analysis is borne out:

- Restaurant A (the cash-only restaurant) has sales of $250,000, but its processing costs are nearly $40,000,59 netting the restaurant $211,250. This restaurant’s processing costs are so high because cash, as outlined in the section on Avoided Cost of Cash, is expensive to handle. For restaurants in particular, cash handling costs are especially high — 15.5%, according to IHL — due to the risks of carrying cash back and forth between tables, the register, and wherever the cash is eventually stored, as well as the risk of theft and miscounting. The cash-only restaurant does not benefit from a boost in sales linked to credit card payments and suffers from a high cost of processing and handling those cash payments, eating away at profitability.

- Restaurant B (the “cash or credit” restaurant), has 70% of the 10,000 monthly payments made by credit cards and 30% made by cash, mirroring the national average according to the Federal Reserve.60 The average transaction size for cash remains the same, $25, but for credit card transactions, the average size is $25.25 because of the 1% incremental lift tied to credit card acceptance (described above in the section on Increased Sales). This restaurant benefits from a higher frequency of credit card payments with a larger ticket size and reduces its processing costs compared to the restaurant that only accepts cash. Credit card payments have an average processing cost of 2.3%, significantly lower than cash.61 Thus, this restaurant generates $251,750 in sales, has processing costs of $15,690, and nets $236,060.

Restaurant C only accepts credit cards and has an average transaction size of $25.25 (due to the incremental lift of credit cards over cash). Therefore, this restaurant generates a higher sales figure than the other two restaurants because of the larger average transaction size on all 10,000 monthly payments. In addition, because this restaurant only accepts credit cards which are cheaper to process, it has lower overall processing costs than the restaurant that only accepts cash and the restaurant that only accepts credit cards and cash. With higher sales ($252,500) and lower processing costs ($5,808), this restaurant generates the highest net total of the three restaurants ($246,693) – a clear example of the benefits of accepting cards over other types of payments.

Table 1: Financial Metrics of Each Restaurant

Restaurant A: Cash Only | Restaurant B: Cash + Credit | Restaurant C: Credit Only | |

Average Cash Transaction | $25 | $25 | N/A |

Average Credit Transaction | N/A | $25.25 | $25.25 |

Share of Transactions: Cash | 100% | 30% | 0% |

Share of Transactions: Credit | 0% | 70% | 100% |

Gross Sales Revenue | $250,000.00 | $251,750.00 | $252,500.00 |

Processing Costs: Cash | $38,750.00 | $11,625.00 | $0 |

Processing Costs: Credit | $0 | $4,065.25 | $5,807.50 |

Total Processing Costs | $38,750.00 | $15,690.25 | $5,807.50 |

Net Sales | $211,250.00 | $236,059.75 | $246,692.50 |

This illustration is not intended to argue that restaurants, or any type of business, should not accept cash as a form of payment. Rather, it is intended to highlight the steep difference in benefits and costs between cash and credit cards and to demonstrate how those benefits and costs could impact revenue and overall processing expenses for a small business. While cash will likely continue to play a role in the economy even as electronic payments become more popular, it is important for businesses to understand the benefits and costs associated with each form of payment and minimize the cost of cash as much as possible to improve profitability.

VI. Conclusion

Retail industry lobbyists often complain that merchants pay “too much” to accept credit cards. In making this argument, however, they typically ignore the benefits that merchants accrue by accepting credit cards, both in terms of the increased revenue that is generated by accepting card payments as well as the reduced costs they would otherwise incur. When the full scope of the costs and benefits associated with accepting credit cards is considered, it is clear that the benefits to merchants easily outweigh the costs. Specifically, by accepting credit cards, merchants accrue roughly $180 billion in net benefits, equivalent to a return of 121% on their credit card processing costs. For merchants, the question is not whether to accept credit cards, but rather how to maximize the use of credit cards given the advantages they provide to store profitability.

Consumer Financial Protection Bureau (2025), “The Consumer Credit Card Market.”

Capital One Shopping Research (2025), “Credit Card Ownership & Usage Statistics.”

Nilson (2025), Issue 1281

Capital One Shopping Research (2025), “Cash vs. Credit Card Spending Statistics.”

Nilson (2025), Issue 1281

IHL Group (2018), “Cash Multipliers: How reducing the costs of cash handling can enable retail sales and profit growth.”

Wall Street Journal (2014), “U.S. Companies Cling to Writing Paper Checks.”

Board of Governors of the Federal Reserve System (2025), “2023 Interchange Fee Revenue, Covered Issuer Costs, and Covered Issuer and Merchant Fraud Losses Related to Debit Card Transactions.”

See, for example, Weisbaum, H. (2011), “Farewell Debit Reward Cards: Banks, Credit Unions Ax Programs In Anticipation of New “Swipe-fee” Rules,” NBC News; McGinnis, P. (2013). Misguided Regulation of Interchange Fees: The Consumer Impact of the Durbin Amendment. Loyola Consumer Law Review Vol. 25 Issue 2-3; Phoenix Consumer Payments Monitor (2013); Pulse (2012), Executive Summary: 2012 Debit Issuer Study, Pulse commissioned Oliver Wyman to conduct its annual 2012 Debt Issuer Study; Manuszak, M. and Wozniak, K. (2017), The Impact of Price Controls in Two-sided Markets: Evidence from US Debit Card Interchange Fee Regulation. Federal Reserve Board

PPI & Robert Shapiro (2025), “The Unanticipated Costs and Consequences of Federal Reserve Regulation of Debit Card Interchange Fees.”

Electronic Payments Coalition (2023), “Out of Balance: How the Durbin Amendment has Failed to Meet Its Promise.”

American Bankers Association Banking Journal (2022), “How Competitive Is The Credit Card Market?”

American Bankers Association (2024), “CFPB analysis obscures truth on credit card market.”

The consulting group Forrester, in their paper titled “The Total Economic Impact Of Commercial Credit Card Acceptance: An Update,” quantified additional benefits of credit card acceptance such as improved debt collection and reduced days sales outstanding amounts. Forrester also noted other benefits that were not quantified in the study, such as improved customer satisfaction, improved visibility into customer payment data, and alignment with third-party self-service tools that help streamline card payment processes.

Nilson (2025), Issue 1281

In the corresponding one pager, EPC calculates the average gross annual benefit for merchants accepting credit cards at $26K. This figure is derived from taking the gross annual benefits ($329B), and dividing by the number of merchants in the U.S. that accept credit cards, approximately 11-14 million. EPC uses the average of 12.5 million merchants to arrive at $26K in benefits per merchant.

Nilson (2025), Issue 1297

Federal Reserve (2025), “2025 Findings from the Diary of Consumer Payment Choice.”

Nilson (2025), Issue 1297

ibid.

Mastercard (2017), “Measuring the Value of Electronic Payments to Merchants.”

Forrester (2024), “The Total Economic Impact of Commercial Credit Card Acceptance: An Update. Cost Savings and Business Benefits Enabled by Commercial Credit Cards.” & Ronald Bird (2024), “How Free Lunch Fallacy Feeds Credit Card Regulation.”

Peter T. Dunn & Company LLC (2018), “The value of electronic payments.” Peter Dunn is a founder of the management consulting firm Edgar, Dunn & Company and provides global advisory services through Peter T. Dunn & Company. He has over 40 years of experience in strategic consulting in payments. Note that Dunn’s 10% assumption is used in a 2016 presentation titled: “Illustrating the Value Provided to United States Merchants by Electronic Payment Products.” In that presentation, Dunn uses internal Mastercard data to arrive at his assumptions and calculations.

Nilson (2025), Issue 1281

Consumer Financial Protection Bureau (2024), “The High Cost of Retail Credit Cards.”

ibid.

ibid.

NRF (2025), “Top 100 Retailers 2025 List.”

30% is an assumption also made by others that have quantified the benefits of credit cards, including Peter Dunn and Forrester. Peter Dunn applied a 30% gross margin when deriving the “Expected Margin on Incremental Sales” benefit of credit cards in his 2016 analysis. Forrester used the same estimate in its analysis on B2B credit card savings. 30% is also in line with New York University’s Stern School of Business “Margins by Sector,” which lists the gross margin for general retail at 32.22%.

IHL Group (2018), “Cash Multipliers: How reducing the costs of cash handling can enable retail sales and profit growth.”

ibid.

ibid.

Nilson (2025), Issue 1281

Nilson (2025), Issue 1297

Federal Reserve (2025), “2025 Findings from the Diary of Consumer Payment Choice.”

Nilson (2025), Issue 1279

- Visa (2025), “Visa Unveils its Scam Disruption Practice, Helping Protect Consumes and the Financial Ecosystem Globally.”

Mastercard (2025), “Securing commerce for all.”

This likely represents a conservative, low estimate of fraud avoided savings for retailers. The estimate does not capture fraud losses reported by the major networks ($4.4 billion in 2024), which could also be considered a benefit to merchants as they are dollars already paid to merchants that are protected by network liability guidelines but absorbed by issuers.

Wall Street Journal (2014), “U.S. Companies Cling to Writing Paper Checks.”

Forrester (2024), “The Total Economic Impact of Commercial Credit Card Acceptance: An Update. Cost Savings and Business Benefits Enabled by Commercial Credit Cards.”

ibid.

Plaid (2025), “ACH Payments 101 – How ACH works for businesses.”

Forrester (2024), “The Total Economic Impact of Commercial Credit Card Acceptance: An Update. Cost Savings And Business Benefits Enabled By Commercial Credit Cards.”

ibid.

ibid.

ibid.

Forrester (2024), “The Total Economic Impact of Commercial Credit Card Acceptance: An Update. Cost Savings And Business Benefits Enabled By Commercial Credit Cards.”

CFPB (2025), “The Consumer Credit Card Market.”

Nilson (2025), Issue 1281

ibid.

NACS (2025), “NACS State of the Industry Report of 2024 Data.”

- ibid.

- ibid.

- ibid.

- ibid.

- ibid.

The Federal Reserve Financial Services (2025), “2025 Findings from the Diary of Consumer Payment Choice.”

IHL Group, “Cash Multipliers: How reducing the costs of cash handling can enable retail sales and profit growth,” 2018.

The Federal Reserve Financial Services (2025), “2025 Findings from the Diary of Consumer Payment Choice.”

Nilson (2025), Issue 1281.